Why Payments Are the Hardest Problem in Social Gaming?

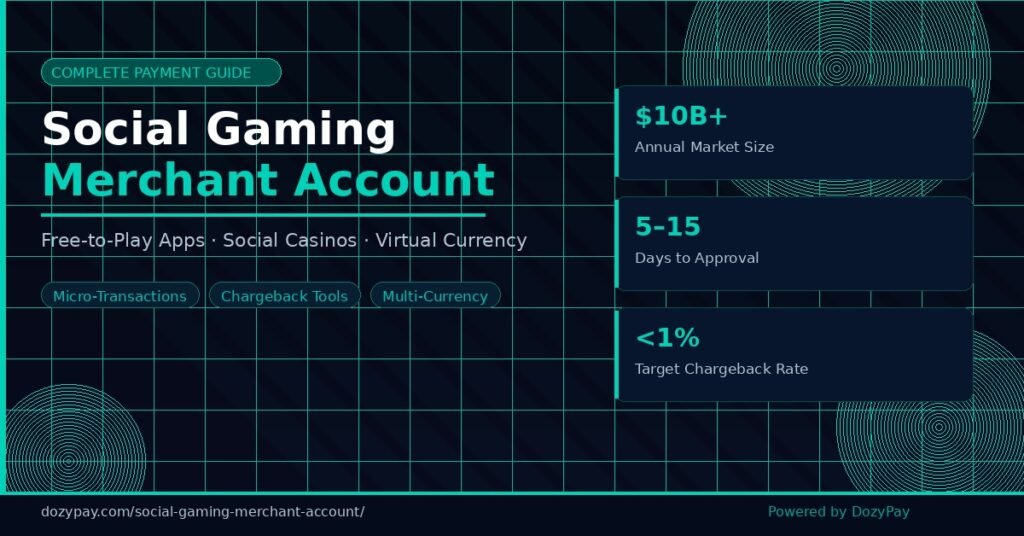

Social gaming is one of the fastest-growing verticals in digital entertainment. Analysts project the global social casino gaming market to exceed $10 billion annually, and free-to-play mobile titles with in-app purchases generate billions more each month.

Yet for all that revenue potential, social gaming businesses hit a wall the moment they try to set up payments.

Standard merchant accounts — the kind e-commerce stores, SaaS companies, and subscription services use — routinely reject social gaming applications. The reason is not the business model itself, but the risk profile that comes with it: high transaction volumes of very small amounts, virtual currency that sits in regulatory grey zones, chargeback rates that consistently exceed industry averages, and compliance requirements that vary dramatically across jurisdictions.

As a result, social gaming businesses typically end up with one of three outcomes:

- A generic high-risk processor that charges excessive fees and offers no industry-specific tooling

- A payment setup patched together from multiple providers, creating reconciliation nightmares

- Or — most commonly — no reliable payment infrastructure at all, leaving significant revenue on the table

This guide changes that. By the end, you will know exactly what a social gaming merchant account is, how it differs from casino and gambling payment processing, what to look for in a provider, and how to get approved quickly.

What Is a Social Gaming Merchant Account?

A social gaming merchant account is a specialised type of merchant account that payment processors configure specifically for businesses operating free-to-play games, social casino applications, or virtual currency platforms.

It differs from a standard merchant account in three critical ways:

1. Risk Classification

Banks and payment processors classify social gaming as high-risk — not because the business is illegal, but because the transaction patterns (micro-transactions, recurring purchases, virtual goods) generate elevated chargeback rates and fraud exposure compared to standard e-commerce. Consequently, processors apply underwriting criteria that standard accounts never encounter.

2. Compliance Requirements

Social gaming platforms must navigate AML (Anti-Money Laundering) rules, KYC (Know Your Customer) obligations, and — depending on jurisdiction — specific virtual currency or sweepstakes regulations. A standard merchant account provider has no framework for this. A social gaming merchant account provider, however, builds exactly this compliance infrastructure into the service.

3. Infrastructure Design

The payment stack for a social gaming business must handle micro-transactions at scale, multi-currency support, recurring billing for premium subscriptions, in-app purchase processing across iOS and Android, and real-time fraud scoring — all simultaneously. Standard accounts simply do not support this workload.

Social Gaming vs. Online Casino vs. Gambling: Understanding the Payment Differences

This is where most business owners get confused — and where getting it wrong costs real money. Social gaming, online casino, and gambling platforms look similar on the surface but carry fundamentally different legal, regulatory, and payment processing implications. Treating them as the same thing leads to account terminations, frozen funds, and compliance violations.

Here is how the three categories differ from a payments perspective:

| Category | Real Money Wagering? | Key Regulation | Payment Risk Level | Best Account Type |

|---|---|---|---|---|

| Social Gaming / Free-to-Play | No | Virtual currency laws, app store policies | Medium-High | Social Gaming Merchant Account |

| Social Casino | No (virtual chips only) | Sweepstakes laws (US), GDPR (EU) | High | Social Gaming Merchant Account |

| Online Casino / Real-Money Gambling | Yes | iGaming licence required | Very High | Casino Merchant Account |

| Sports Betting / Gambling | Yes | Gambling Act (varies by country) | Very High | Gambling Payment Gateway |

The distinction matters enormously when applying for a merchant account. A social casino platform that processes no real-money wagering carries a fundamentally different compliance profile than a real-money online casino — and therefore needs a different account type with different underwriting criteria.

If you operate a real-money casino, you need a casino merchant account designed for iGaming operators. If you run a gambling platform that handles sports betting or poker, a dedicated gambling payment gateway is the correct infrastructure. For social gaming — free-to-play, virtual chips, in-app purchases — the social gaming merchant account is the right fit. Applying for the wrong type is one of the most common and costly mistakes in this vertical.

The 6 Core Payment Challenges Unique to Social Gaming Platforms

Understanding what makes social gaming payments hard is the foundation for choosing the right provider. Here are the six challenges every platform faces:

Challenge 1: Micro-Transaction Volume at Scale

Free-to-play games build their monetisation around frequent, small purchases — $0.99 for a coin pack, $4.99 for a premium skin, $1.99 for an extra life. A mid-sized social gaming platform processes tens of thousands of these transactions every day. Standard processors optimise for lower-volume, higher-value transactions and often throttle or flag accounts that generate unusual micro-transaction patterns.

A purpose-built social gaming merchant account, by contrast, undergoes underwriting specifically for this transaction profile — high volume, low average order value — so the payment infrastructure does not mistake normal business activity for fraud.

Challenge 2: Virtual Currency Complexity

Virtual currencies — coins, gems, tokens, credits — occupy a regulatory grey zone in most jurisdictions. They are not real money, but players purchase them with real money, and some platforms allow exchanges or uses that attract regulatory scrutiny.

Payment processors therefore need a clear framework for handling virtual currency transactions. Without one, platforms face account holds, forced refunds, or terminations triggered by compliance teams that do not understand the virtual goods model.

Challenge 3: Chargeback Exposure

Social gaming platforms consistently see higher chargeback rates than most digital businesses. The reasons are specific to the industry: buyers’ remorse on virtual goods (which players cannot “return”), shared family devices where parents dispute children’s purchases, and friendly fraud from players who claim they did not authorise a transaction after spending the virtual goods.

Without chargeback management tooling — real-time alerts, automated dispute responses, velocity controls — social gaming platforms breach the 1% chargeback threshold that card networks set, which triggers account termination or inclusion in MATCH and VMAS blacklists.

Challenge 4: Global Player Base, Local Payment Preferences

Social gaming is inherently borderless. A mobile title launched in the UK attracts players from Germany, Brazil, Indonesia, and the United States within weeks. Each market has different preferred payment methods: credit cards dominate in the US, but iDEAL leads in the Netherlands, PIX in Brazil, UPI in India, and e-wallets across Southeast Asia.

A payment infrastructure that only accepts Visa and Mastercard leaves a significant percentage of global revenue uncollected. The right social gaming merchant account, accordingly, includes multi-currency processing and alternative payment method (APM) support out of the box.

Challenge 5: App Store Payment Splitting

Platforms on iOS App Store or Google Play face a dual-payment reality: in-app purchases that go through the app store (subject to Apple/Google’s 15–30% commission) and direct web purchases that go through their own merchant account (no commission). Managing both payment flows, reconciling them accurately, and staying compliant with app store policies requires a payment provider that understands the social gaming distribution model.

Challenge 6: Recurring Billing for Premium Tiers

Most social gaming platforms layer a subscription model on top of their free-to-play base — a “VIP” or “Premium” tier offering ad-free play, bonus currency, or exclusive content. Processing recurring billing reliably, handling subscription upgrades and downgrades, and managing failed payment recovery are all infrastructure requirements that standard processors handle poorly.

What to Look for in a Social Gaming Merchant Account Provider?

Not all high-risk payment processors have the tools and experience that social gaming platforms need. Here is the checklist every platform should use when evaluating providers:

Specialist Underwriting

The underwriting team should carry direct experience with social gaming, virtual currency, and free-to-play business models. Generic high-risk underwriters apply blanket risk controls that other industries need — controls that create unnecessary declines and excessive hold periods for social gaming.

Chargeback Management Tools

Real-time chargeback alerts (Ethoca, Verifi), automated dispute response workflows, and velocity controls that flag suspicious purchase patterns before they become chargebacks are non-negotiable for social gaming platforms.

Multi-Currency and APM Support

Providers should support 50+ currencies and at least the major alternative payment methods in your key markets (PayPal, Apple Pay, Google Pay, local bank transfers, e-wallets). Global revenue depends on meeting players where they prefer to pay.

Micro-Transaction Optimisation

The processor’s infrastructure must handle high-volume, low-value transactions without throttling or triggering fraud flags. Before applying, ask specifically whether their system supports micro-transaction profiles.

Real-Time Fraud Scoring

Machine learning-based fraud detection that operates in real time — not batch review — is essential for social gaming. Compromised player accounts and carding attacks generate transaction patterns that processors must catch before the transaction completes, not after.

Developer-Friendly Integration

A well-documented REST API, SDKs for iOS and Android, and pre-built plugins for Unity and Unreal Engine reduce integration time from weeks to days. Always ask for API documentation before signing any agreement.

Transparent Fee Structure

Social gaming payment processing fees should clearly break down into: interchange, processor markup, chargeback fees, rolling reserve percentage, and payout schedule. Providers who bundle everything into a single opaque percentage almost always cost more than they initially appear.

Compliance Support

AML screening, KYC workflows for high-value purchasers, and regulatory guidance for your key markets should come as standard — not as a billed add-on.

How the Approval Process Works: Getting Your Social Gaming Merchant Account?

The application process for a social gaming merchant account is more involved than a standard merchant account, but significantly less complex than a real-money casino or gambling account. Here is what to expect at each stage:

Step 1: Business Documentation

Prepare your business registration documents, directors’ ID verification, bank statements (3–6 months), and — critically — a clear description of your business model that explicitly distinguishes your platform from real-money gambling. Underwriters must see this distinction in writing.

Step 2: Platform Review

The underwriter will review your platform — website, app, terms of service, and privacy policy. Your terms of service must clearly state that virtual currency carries no real-money value and is non-refundable. Additionally, your privacy policy must comply with GDPR and CCPA requirements.

Step 3: Transaction History

If you have existing processing history, provide up to 12 months of statements. Processors want to see your average transaction value, monthly volume, and — most importantly — your chargeback ratio. A chargeback rate below 0.5% is ideal; above 1%, you need to supply an explanation and a documented remediation plan.

Step 4: Financial Review

Underwriters assess financial stability, revenue projections, and rolling reserve requirements. Newer platforms without processing history typically face a rolling reserve (5–10% of monthly volume for 90–180 days) that the processor releases once you establish a track record.

Step 5: Compliance Review

The underwriter reviews AML and KYC policies, virtual currency terms, and geographic restrictions on player access. Having documented internal compliance policies significantly accelerates this stage.

Step 6: Approval and Integration

Approval timelines for social gaming merchant accounts typically run 5–15 business days. Once approved, integration via API or SDK is the final step before going live.

Virtual Currency Compliance: What Every Platform Needs to Know

Virtual currency is the operational core of social gaming monetisation — and the area most likely to create compliance problems without the right documentation. Here are the key rules every platform should document before processing begins:

Define Your Virtual Currency Clearly

Your terms of service must specify that virtual currency (coins, gems, tokens, credits) carries no monetary value, cannot be withdrawn as cash, and is not transferable between accounts. This definition is the primary distinction between a social gaming platform and a gambling operation in most jurisdictions.

Understand Sweepstakes Law in the US

Social casino platforms that offer “sweepstakes coins” — purchasable virtual currency for prize-eligible play — operate under US sweepstakes law, not gambling law. However, this only holds if the platform meets specific no-purchase-necessary requirements. Payment processors must understand your sweepstakes structure before they underwrite your account.

Build Age Verification In From Day One

Even for platforms with no real-money wagering, app stores, regulators, and payment processors increasingly require age gates and age verification workflows. Build this into your compliance stack from the start.

GDPR and CCPA Compliance

Player payment data qualifies as personal data under both GDPR (EU) and CCPA (California). Your data processing agreements with your payment provider must meet these standards, and your privacy policy must disclose how you collect, store, and use payment data.

Social Gaming Payment Processing Fees: What’s Normal, What’s Excessive?

Processors classify social gaming as high-risk, which means processing fees run higher than standard e-commerce. However, there is a significant range across providers, and understanding what is normal prevents overpaying.

| Fee Component | Standard E-Commerce | Social Gaming (High-Risk) | Red Flag |

|---|---|---|---|

| Interchange + Markup | 1.5–2.5% | 2.5–4.5% | Above 5% |

| Chargeback Fee | $15–$25 | $25–$50 | Above $75 |

| Rolling Reserve | None | 5–10% / 90–180 days | Above 15% |

| Monthly Fee | $0–$25 | $25–$75 | Above $150 |

| Setup Fee | $0 | $0–$500 | Above $1,000 |

| Refund Fee | $0 | $5–$15 | Above $25 |

The most important fee to negotiate is the rolling reserve — both the percentage and the release timeline. As your processing history matures, a good provider will reduce or eliminate the reserve. If a provider refuses to commit to a reserve reduction schedule, treat that as a red flag.

DozyPay’s Social Gaming Merchant Account: What’s Included

DozyPay builds its social gaming merchant account specifically for the free-to-play, social casino, and virtual currency space. Rather than retrofitting a generic high-risk solution, DozyPay designs this infrastructure from the ground up around the actual transaction patterns and compliance requirements of social gaming platforms.

Key capabilities include:

- Micro-transaction optimisation — infrastructure that handles high-volume, low-value transaction profiles without throttling or false-positive fraud flags

- Multi-currency processing — support for 100+ currencies and major alternative payment methods across all key gaming markets

- Real-time fraud scoring — machine learning-based fraud detection at transaction level, with velocity controls that we calibrate specifically for gaming behaviour patterns

- Chargeback management — Ethoca and Verifi integration, automated dispute workflows, and proactive chargeback alerts

- Recurring billing — full subscription management, failed payment recovery, and dunning automation for premium tier monetisation

- Developer-first API — REST API with SDKs for iOS, Android, Unity, and Unreal Engine; average integration time under 5 business days

- Compliance support — AML screening, KYC workflows, virtual currency compliance review, and regulatory guidance, all included as standard

For platforms that also operate real-money casino products alongside a social gaming vertical, DozyPay’s online casino payment gateway handles the iGaming side — allowing operators to manage both payment streams under a single provider relationship.

Common Mistakes Social Gaming Platforms Make With Payments

Mistake 1: Applying With a Standard Merchant Account

The fastest way to trigger an account termination is to process social gaming transactions through a standard merchant account without disclosing your business model. The elevated chargeback rate will trigger automated risk reviews within weeks.

Mistake 2: Not Distinguishing Your Platform From Gambling in Your Terms

Underwriters, regulators, and card networks all draw a legal line between social gaming and real-money gambling. If your terms of service do not explicitly mark that distinction, your account remains vulnerable to review or termination.

Mistake 3: Underestimating the Chargeback Problem

First-time social gaming operators routinely underestimate how much chargeback management matters. Proactive tools — not reactive dispute responses — are what keep chargeback ratios below the threshold.

Mistake 4: Single-Provider Dependency

Running your entire payment infrastructure through a single processor creates a single point of failure. A secondary processor for high-value markets significantly reduces downtime risk.

Mistake 5: Ignoring Alternative Payment Methods

Limiting payment options to Visa and Mastercard leaves 20–40% of potential revenue uncollected in markets like Brazil, India, Germany, and Southeast Asia. APM support is not optional for a global platform.

Frequently Asked Questions

Is a social gaming merchant account the same as a casino merchant account?

No. A social gaming merchant account serves platforms where no real money changes hands — virtual chips, in-app purchases, and virtual currency only. A casino merchant account serves real-money iGaming operators who hold gambling licences. Applying for the wrong account type leads to rejection or compliance violations.

How long does it take to get approved?

For social gaming specifically, approval typically takes 5–15 business days with a complete application package. Platforms with clean processing history and documented compliance policies move through faster.

What chargeback rate is acceptable for a social gaming platform?

Card networks set 1% as the threshold above which they place accounts under review or terminate them. Social gaming platforms should target below 0.7% with active chargeback management tools. Above 1%, Visa’s VMAS or Mastercard’s MATCH programme applies — and that makes future account approvals very difficult.

Do I need a gambling licence for a social casino platform?

In most jurisdictions, no — provided your platform involves no real-money wagering and meets sweepstakes law requirements where applicable. However, regulatory requirements vary significantly by country and change frequently. Always take legal advice for your specific markets.

Can I process payments for players in the United States?

Yes, subject to compliance with US consumer protection laws, app store policies, and — for sweepstakes-based social casinos — state sweepstakes regulations. Some states have specific restrictions. Your payment provider’s compliance team should advise on US market requirements specifically.

What happens to funds during the rolling reserve period?

The processor holds rolling reserve funds as a risk buffer against chargebacks and refunds. Importantly, the processor holds these funds — does not forfeit them — and releases them to you on a rolling basis, typically after 90–180 days. Both the reserve percentage and the release timeline are negotiable, and both should decrease as your processing history matures.

Conclusion: The Right Payment Foundation Changes Everything

Social gaming is a high-margin, high-growth business. Without a payment infrastructure that matches the transaction patterns, compliance requirements, and risk profile of the industry, however, revenue leaks are inevitable — through failed transactions, account terminations, excessive fees, and chargebacks.

The right social gaming merchant account is not just a payment processor. It is a risk management partner, a compliance infrastructure, and a revenue optimisation tool — all in one.

DozyPay builds its social gaming merchant account specifically for free-to-play apps, social casinos, and virtual currency platforms that need reliable, scalable payment processing. Furthermore, it removes the overhead of managing multiple providers or navigating compliance blind spots alone.

If you are ready to get your payment infrastructure right from the start — or fix a payment stack that is costing you revenue — request a quote and our team will respond within one business day.

DozyPay is a specialist high-risk payment gateway and merchant account provider, helping businesses in 150+ countries accept payments securely and without interruption. Our team includes payment analysts, compliance specialists, and fintech professionals with over a decade of combined experience in high-risk merchant processing — covering industries such as IPTV, adult content, online gaming, forex trading, pharmaceuticals, and travel.

Every article published by DozyPay is researched and written by our in-house payments team, drawing on real underwriting experience, industry data, and direct merchant feedback. Our goal is simple: give high-risk business owners the clear, honest information that banks and mainstream processors won’t.