Introduction: Why Chargebacks Are the Silent Killer of Casino Merchant Accounts?

The Cost of Getting This Wrong

If you operate an online casino, gaming platform, or social gaming site, chargebacks are not just a payment problem. They are an existential threat to your casino merchant account. When your chargeback ratio climbs above 1%, acquiring banks begin reviewing your account. Cross 2%, and they terminate it.

Termination creates a lasting problem. Processors become difficult to find. Opening a new casino merchant account costs more and takes longer. Some card networks place terminated merchants on the MATCH list, blocking standard processing for up to five years.

Who Faces the Highest Risk?

Operators running a casino merchant account for high risk business face this problem most sharply. Card-not-present fraud, friendly fraud, and unclear billing descriptors all converge here to produce chargeback rates unthinkable in low-risk verticals.

Casino merchant account for small business operators face equal pressure. Their margins are tighter. A single chargeback spike triggers account reviews that can paralyse operations — with no large reserve to absorb the impact.

Prevention Over Reaction

Chargebacks are not inevitable. They are largely preventable. Preventing them requires a systematic approach rather than isolated fixes. That is exactly what this six-step framework delivers.

Already holding a processing relationship? Then start implementing this framework today. Still researching how to get a casino merchant account, build chargeback prevention into your operations from day one. It is the single most important factor in keeping that account active, healthy, and growing.

Industry Context — Why This Matters Now

| 1.8% Average chargeback rate in online gambling — 3x higher than e-commerce | 86% Of gambling chargebacks involve friendly fraud — not genuine card theft | $40 Average true cost per chargeback when fees, labour, and lost revenue combine |

What Exactly Is a Chargeback — and Why Do Casino Operators Get More of Them?

The Mechanics of a Chargeback

A chargeback occurs when a cardholder disputes a transaction with their issuing bank. The merchant is bypassed entirely. Unlike a refund — which you initiate — the card network imposes a chargeback on you. The bank reclaims the transaction amount from your settlement and adds a penalty fee. The incident also counts against your merchant account ratio.

Casino and gambling operators attract disproportionately high chargeback rates for several well-documented reasons. The table below summarises the most common causes:

| Root Cause | Why It Happens in Gambling |

| Friendly Fraud | Players dispute charges after losing. They claim they ‘did not authorise’ the deposit. Buyer’s remorse chargebacks run far higher here than in retail. |

| Unrecognised Descriptors | The billing descriptor reads ‘PRTNR-GMBLD2948’ instead of your brand name. The player contacts their bank rather than you. |

| Multiple Rapid Deposits | Players deposit several times in one session. When they dispute, they dispute every transaction — multiplying your chargeback count instantly. |

| Account Takeover Fraud | A fraudster accesses a player’s account and deposits using stolen card details. The legitimate cardholder then disputes all the charges. |

| Unclear Cancellation Process | Players cannot easily stop recurring charges or find your support contact. They call their bank instead of calling you. |

| Shared Household Cards | A family member discovers gambling charges made by another household member and disputes them as unauthorised. |

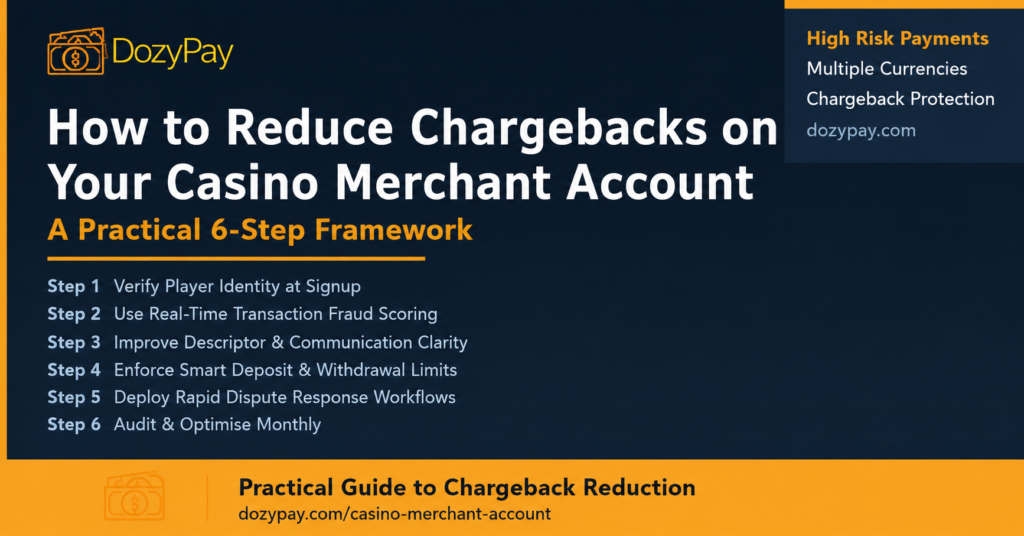

The 6-Step Chargeback Reduction Framework for Casino Merchant Accounts

Payment processors who specialise in casino merchant accounts for high risk business developed this framework from direct operational experience. Each step targets a distinct vulnerability in the payment lifecycle. Together, they create a layered defence. Apply them consistently and expect a 60–80% chargeback reduction within 90 days.

STEP 1 Verify Player Identity at Signup — Not After a Dispute

Why Upfront KYC Stops Chargebacks Before They Start?

Robust Know Your Customer (KYC) verification at signup is the single most effective chargeback prevention measure — before a player makes their first deposit. Operators who delay KYC until a withdrawal request or a dispute expose themselves to friendly fraud. They hold no proof of authorisation.

Completing identity verification at signup achieves three things at once. First, you obtain documented proof that the account holder and the cardholder are the same person. Second, you signal to the player that your platform takes verification seriously — deterring anyone planning a future dispute. Third, you build an evidentiary trail that wins disputes when they do occur.

Minimum KYC Requirements for Casino Merchants

- Government-issued photo ID (passport or national ID) verified before first deposit

- Address verification using a utility bill, bank statement, or automated database check

- Card verification — require a photograph of the card used (first 6 and last 4 digits visible, CVV covered) or use a processor that provides 3D Secure 2.0 authentication

- Email and mobile number verification via OTP at account creation

- Terms and conditions acceptance with a recorded timestamp and IP address — essential evidence in dispute responses

Automation Options for Small Business Operators

For operators running a casino merchant account for small business, manual KYC review may not scale. Partner with a processor — such as DozyPay — that provides automated KYC-as-a-service built directly into your payment flow. Compliant players pass through invisibly. High-risk profiles get flagged before they deposit.

Also enable 3D Secure 2.0 (3DS2) for all card transactions. When authentication succeeds, liability shifts from you to the issuing bank. Even if a player later disputes the transaction, the bank absorbs the loss. This single change eliminates a significant portion of friendly fraud chargebacks.

STEP 2 Use Real-Time Transaction Fraud Scoring on Every Deposit

Beyond Friendly Fraud: Card Theft and Account Takeover

Not all chargebacks stem from friendly fraud. A material proportion come from genuine card theft and account takeover. This is especially true on platforms supporting cryptocurrency-to-card flows or high-velocity deposit patterns. and account takeover. These produce the most damaging chargebacks. The legitimate cardholder is blameless, the bank wins the dispute easily, and the transaction amount is often large.

Preventing this category requires real-time fraud scoring. The system assesses each transaction’s risk profile before authorisation — not after settlement.

Key Fraud Signals Your Payment Stack Should Monitor

- Velocity checks — multiple deposits from the same card in a short window, or one card used across multiple accounts

- Device fingerprinting — a new card used from a device that previously used a declined or disputed card

- IP geolocation — the player’s stated location and their IP location diverge significantly, or the IP resolves to a high-fraud jurisdiction

- BIN analysis — certain card prefixes carry significantly higher dispute rates; real-time BIN scoring applies enhanced friction to high-risk cards

- Behavioural analytics — abnormally fast deposit sequences or deposits placed immediately after account creation are strong fraud indicators

When you apply to get a casino merchant account through a specialist processor, ask explicitly about their fraud scoring infrastructure. DozyPay’s casino merchant account solution includes real-time transaction screening through an integrated risk engine. You set custom thresholds that balance fraud prevention with player experience.

STEP 3 Fix Your Billing Descriptor and Player Communication

The Cheapest Chargeback Fix Available

This step demands the least technical investment but delivers some of the fastest results. Industry estimates put 25–35% of gambling chargebacks down to one cause: the player does not recognise the charge on their statement.

The player deposits on a branded casino platform. Their bank statement, however, shows something like ‘MLTPAY-GMBLDG-0249’ or ‘PARTPAY LTD UK’. They do not recognise it. They assume fraud. They call their bank and file a dispute. One descriptor configuration change prevents this entirely.

Billing Descriptor Best Practices

- Use your brand name, not your processor’s name — configure a custom dynamic descriptor that displays your platform’s name

- Include a short contact method in the descriptor — ‘DOZYCASINO 0800-XXX’ is immediately recognisable and gives the player a resolution path before they call their bank

- Send a post-deposit email confirmation within seconds — include the exact amount, a transaction reference, and a clear ‘Contact Us’ link. This step alone cuts ‘I don’t recognise this charge’ disputes dramatically

- Send a deposit confirmation push notification if your platform has a mobile app — reinforcing the transaction in the player’s mind at the moment of deposit

- For recurring charges, send a reminder 3 days before each charge — include the amount, date, and an easy cancellation link

Multi-Currency Descriptor Consistency

Operators supporting casino merchant account multiple currencies must apply this strategy uniformly across all currency streams. A player depositing in EUR, GBP, or AUD should see the same recognisable brand descriptor as your USD-denominated players. Currency inconsistencies in descriptors trigger chargebacks specifically in multi-currency casino operations.

STEP 4 Enforce Smart Deposit Limits and Withdrawal Policies

Two Patterns That Drive Disproportionate Chargebacks

Two operational patterns generate a disproportionate share of casino chargebacks: unlimited deposit velocity and delayed or difficult withdrawals. Address both simultaneously. A structured deposit limit framework combined with a clear, fast withdrawal process reduces chargebacks and strengthens player trust.

Deposit Limit Strategy

- Implement session deposit limits that require explicit player action to increase — rather than allowing unlimited consecutive deposits by default. This reduces transaction exposure per session.

- Apply graduated deposit caps for new or recently verified accounts. For example, enforce a 48-hour cooling-off period before a new player can raise their limit above a baseline. This window carries your highest fraud risk.

- Multi-currency operators should set per-currency limits. Each payment corridor carries a different risk profile, and limits should reflect that. Dispute rates vary significantly by country and card network.

- Require re-authentication (email OTP or 2FA) before processing deposits above a defined threshold. This creates additional authorisation proof and deters friendly fraud by raising the evidentiary bar.

Withdrawal Process Strategy

- Process withdrawal requests within 24 hours wherever possible. Delayed withdrawals are a primary chargeback trigger. Players who cannot retrieve funds through your platform seek them through their bank.

- Send a withdrawal confirmation email immediately — include the expected processing time and a tracking reference. Managing player expectations proactively prevents disputes that arise from uncertainty.

- Offer multiple withdrawal methods, not just the deposit method. Players who deposited by card but can only withdraw by card face unnecessary friction. Supporting bank transfer, e-wallets, and where appropriate, cryptocurrency, reduces this friction substantially.

- Publish a clear refund and withdrawal policy on your platform. Link it from every deposit confirmation email. Make it accessible with one click from the player dashboard.

Operators processing through DozyPay’s gambling payment gateway benefit from multi-currency settlement and rapid withdrawal processing built into the core platform — directly addressing the withdrawal friction that drives preventable chargebacks.

STEP 5 Build a Rapid Dispute Response Workflow Before You Need It

Why Preparation Determines Win Rate?

When a chargeback arrives, you typically have 7–14 days to submit a representment before the deadline passes. Miss it, and the chargeback stands automatically. Operators without a documented process nearly always miss deadlines or submit weak evidence. They lose disputes they could have won.

Build your dispute response workflow before disputes arrive — not after. This separates operators who recover 40–60% of disputed transactions from those who recover under 10%.

Your Dispute Response Pack Should Include

- KYC verification records — proof that you verified the cardholder against a government-issued ID before their first deposit

- Signed or accepted terms and conditions — a timestamped record of the player accepting your T&Cs at account creation, including the clause covering deposits and refunds

- Transaction history — a complete log of all deposits and withdrawals by the player, demonstrating an established transactional relationship

- Login and session logs — IP address, device fingerprint, geolocation, and timestamp for the disputed session, showing the transaction came from the player’s known device and location

- 3DS2 authentication confirmation — if 3D Secure was in use, include the authentication reference and the liability shift confirmation from your processor

- Communication records — any emails, chat transcripts, or support tickets between your team and the player related to the disputed transaction

- Deposit confirmation email — proof that you sent a transaction confirmation to the player’s verified email at the time of the deposit

Organising and Scaling Your Evidence

Organise this evidence into a single, clearly structured PDF for each dispute. Your casino merchant account provider should supply templates for the Visa and Mastercard dispute codes most common in gambling — typically EC/4853 (Services Not as Described) and UA02 (Fraud Card-Not-Present).

Consider using a chargeback management service or dispute automation tool if your volume exceeds 20–30 disputes per month. The recovered revenue typically covers the tool cost many times over.

STEP 6 Audit Your Chargeback Data Monthly and Optimise Continuously

Why Chargeback Prevention Is an Ongoing Discipline?

The five steps above create a strong baseline defence. Chargeback patterns evolve, however, as fraud tactics change, player demographics shift, and your platform grows. Operators who maintain ratios below 0.5% treat chargeback reduction as an ongoing discipline. They never treat it as a one-time implementation project.

A monthly audit serves three purposes. It identifies emerging patterns. These include new fraud vectors, game types with high dispute rates, and payment methods with elevated ratios. It provides data for productive conversations with your processor about risk scoring adjustments. It also demonstrates to your acquiring bank that you actively manage chargeback exposure. Banks reward this with favourable processing terms.

Monthly Audit Checklist

- Chargeback ratio by card type: Visa and Mastercard dispute rates can diverge significantly. An elevated rate on one network usually points to specific BIN ranges or dispute code patterns.

- Dispute reason code breakdown: Categorise disputes by reason code — fraud (UA02, 10.4), service disputes (4853, 13.1), and processing errors. Each category needs a different prevention response.

- Top 10 disputing player segments: Find whether disputes cluster around specific acquisition channels, geographies, deposit methods, or game types. This data shows where prevention effort delivers the most value.

- Win rate on representments: Track the percentage of disputes you win on representment. A win rate below 30% typically signals evidence quality problems in your response pack.

- Dispute lag analysis: Measure the average time between the original transaction and the dispute filing date. Long lags (90+ days) often indicate friendly fraud. Short lags (under 7 days) often indicate card theft or account takeover.

- Multi-currency dispute breakdown: For casino merchant account multiple currencies operations, analyse dispute rates by currency and region. Certain markets carry structurally higher chargeback rates that require enhanced controls or alternative payment methods.

- Processor communication: Share your monthly audit results with your payment processor. Processors who specialise in casino merchant account for high risk business verticals use merchant data to fine-tune risk scoring. DozyPay, for example, adjusts thresholds based on your specific patterns.

How Chargeback Ratios Affect Your Casino Merchant Account Status

Understanding the Threshold System?

Every operator should understand the threshold system that banks and card networks apply — whether you are working out how to get a casino merchant account for the first time or managing an established processing relationship.

| Chargeback Ratio | Status | Processor/Bank Action |

| Below 0.5% | Healthy | No intervention. Lowest processing fees. Best terms for new payment methods and currencies. |

| 0.5% – 1.0% | Monitoring | Processor may issue an advisory notice. Your account stays active but gets flagged for increased scrutiny. |

| 1.0% – 2.0% | Early Warning | Visa and Mastercard dispute monitoring programmes activate. Your processor requires a remediation plan. |

| Above 2.0% | Critical | Account suspension or termination becomes likely. Card network fines apply. MATCH list placement may block new merchant accounts for 5 years. |

The Multi-Currency Ratio Calculation

Note that casino merchant account multiple currencies operations receive chargeback ratio assessments per card network — not per currency. A high dispute rate in a single currency corridor can still trigger monitoring programme actions. For example, elevated disputes from UK-issued cards can breach Mastercard or Visa per-network thresholds — even if your USD processing stays clean.

How to Get a Casino Merchant Account with Strong Chargeback Controls Already Built In?

Evaluating Processors on Chargeback Infrastructure

If you are in the research phase, the chargeback control infrastructure of a potential processor should rank among your primary evaluation criteria. Not all high-risk processors are equal here, and the differences in outcomes are significant. Ask these specific questions when researching how to get a casino merchant account:

- Does your platform include 3D Secure 2.0 for all card transactions? Do you support liability shift documentation for dispute responses?

- What fraud scoring tools run at the transaction level — and can merchants customise the thresholds?

- Do you support dynamic billing descriptors with brand name configuration? Can you display a contact URL in the descriptor?

- What chargeback management support do you provide? Do you have a dedicated dispute response team? What is your average representment win rate in gambling verticals?

- Do you support casino merchant account multiple currencies with per-currency chargeback monitoring and reporting?

- What happens when my chargeback ratio exceeds 1%? Do you offer a remediation programme, or do you suspend the account immediately?

Why Specialist Processors Outperform Generalists?

DozyPay’s casino merchant account solution covers all of the above. Integrated 3DS2, real-time fraud scoring, multi-currency chargeback monitoring, and a dedicated dispute management team keep your chargeback ratio in the healthy range from day one.

The same infrastructure scales with you. It works whether you run a casino merchant account for small business processing your first thousand transactions or an established platform handling millions in monthly volume. The infrastructure scales with you.

Special Considerations: Chargebacks on Casino Merchant Account Multiple Currencies Operations

Currency Conversion Disputes

Operators running casino merchant account multiple currencies environments — accepting EUR, GBP, CAD, AUD, and other major currencies alongside USD — face a distinct set of chargeback challenges. The conversion rate at the time of a dispute may differ from the rate at the time of the deposit. This creates legitimate confusion about the charged amount and occasional disputes from players who missed a conversion notification at checkout. Mitigate this by displaying the estimated billing currency amount at deposit. Include the same figure in the confirmation email.

Regional Friendly Fraud Patterns

Chargeback propensity varies significantly by geography. Certain markets carry structurally higher chargeback risk. The UK, Australia, and Germany all have consumer protection frameworks that make it straightforward for cardholders to file disputes with minimal bank scrutiny. For these markets, enforce enhanced KYC, lower deposit velocity limits, and stronger 3DS2 enforcement from the outset.

Acquiring Bank and Network Rules by Jurisdiction

Visa and Mastercard apply chargeback rules per network and per region. The time windows for representment, the burden of evidence, and the available reason codes all differ between regions. Choose a processor with specific expertise in the dispute rules for each currency corridor you process. This expertise is a key advantage of using a specialist like DozyPay over a generalist processor for your casino merchant account multiple currencies needs.

Chargeback Management for Casino Merchant Account Small Business Operators

The Small Operator Advantage

Running a casino merchant account for small business — whether a niche social gaming platform, a boutique online casino, or a new market entrant — means fewer resources than large platforms but equal chargeback exposure. However, small operators hold one significant advantage: agility. A large platform may take months to implement a new fraud rule or update a KYC workflow. A small team can deploy the same change in days. Use that speed.

Specific Priorities for Small Business Casino Operators

- Start with KYC automation, not manual review: Manual KYC does not scale and creates approval delays that frustrate legitimate players. Integrate automated KYC from day one through your processor.

- Use your processor’s fraud tools fully: A casino merchant account for small business typically includes access to the same fraud scoring tools available to large operators. Many small operators skip configuration. Spend time setting thresholds and reviewing fraud alerts — the initial effort prevents significantly larger losses later.

- Respond to every dispute personally at first: In early operations, review each dispute individually rather than relying on templates. The patterns you spot in your first 50 disputes will teach you more about your specific chargeback drivers than any general framework.

- Use your rolling reserve strategically: Most processors require a rolling reserve for high-risk casino merchant accounts. Treat it as your chargeback buffer. Use it as motivation to reduce your ratio quickly and negotiate a lower reserve percentage.

Frequently Asked Questions:

What chargeback ratio causes a casino merchant account to face termination?

Both Visa and Mastercard trigger formal monitoring programmes at a 1% chargeback ratio. The threshold requires 100 or more disputes in a calendar month. Termination risk rises sharply above 2%. Acquiring banks that specialise in casino merchant accounts for high risk business typically step in earlier — often at 0.75–1% — with remediation requirements before card network programmes activate.

How quickly can I reduce my chargeback ratio after implementing these steps?

Operators who implement all six steps simultaneously typically see measurable improvement within 30 days. A 50–70% reduction usually follows within 90 days. Fixing billing descriptors and deploying 3DS2 produce the fastest wins — often within 1–2 weeks. KYC and fraud scoring improvements take 4–8 weeks to show statistical impact. The monthly audit discipline then drives continuous improvement beyond the initial implementation period.

Can I dispute and win chargebacks in the gambling vertical?

Yes, and consistently so when you hold strong evidence. Operators with complete KYC records, 3DS2 authentication, session logs, and communication records regularly win 50–65% of disputed transactions. Organising this evidence in advance determines your win rate. Submitting it quickly seals the outcome. That is why Step 5 is non-negotiable.

What is the difference between a refund and a chargeback — and which should I offer?

A refund is merchant-initiated. It costs you the transaction amount plus standard processing fees. A chargeback costs you the transaction amount plus a penalty fee of typically $20–$40. It also adds a count against your ratio and consumes significant administrative time. When a player raises a dispute concern, offer a proactive refund. It is almost always the better economic choice — even when you believe you would win.

Does supporting multiple currencies increase my chargeback risk?

Operating a casino merchant account multiple currencies environment does not inherently increase chargeback risk. It increases complexity — specifically around descriptor clarity, conversion transparency, and jurisdiction-specific dispute rules. Operators who address these factors explicitly maintain chargeback ratios equivalent to single-currency platforms.

How does DozyPay help casino merchants manage chargebacks?

DozyPay’s casino merchant account platform includes integrated real-time fraud scoring, 3DS2 authentication, custom billing descriptor configuration, multi-currency chargeback monitoring, and a dedicated dispute management team with deep expertise in gambling vertical reason codes. DozyPay’s gambling payment gateway engineers chargeback reduction into the architecture — not as a bolt-on feature.

Conclusion: Chargebacks Are Manageable — With the Right System

A Systems Problem With a Systems Solution

A high chargeback ratio is not an industry inevitability for casino and gambling operators. It is a systems problem — and systems problems have systems solutions. The six-step framework targets every major chargeback source in the gambling vertical. These include identity fraud, billing confusion, deposit velocity, withdrawal friction, weak dispute responses, and reactive monitoring.

Whether you manage an existing casino merchant account for high risk business, build chargeback controls into a new casino merchant account for small business, or evaluate processors while learning how to get a casino merchant account for the first time — the principles apply equally. Verify early, score transactions in real time, communicate clearly, limit exposure, respond to disputes rapidly, and audit monthly.

The Platform Makes the Difference

When you implement these steps through a processor built for the gambling vertical — one that supports casino merchant account multiple currencies, integrated fraud tools, and proactive chargeback management — you have everything you need to maintain a healthy ratio and keep your merchant account operating at full capacity.

Ready to reduce chargebacks on your casino merchant account?

DozyPay provides specialist high-risk payment solutions for casino and gambling operators.

Apply at: dozypay.com/casino-merchant-account

Email: contact@dozypay.com