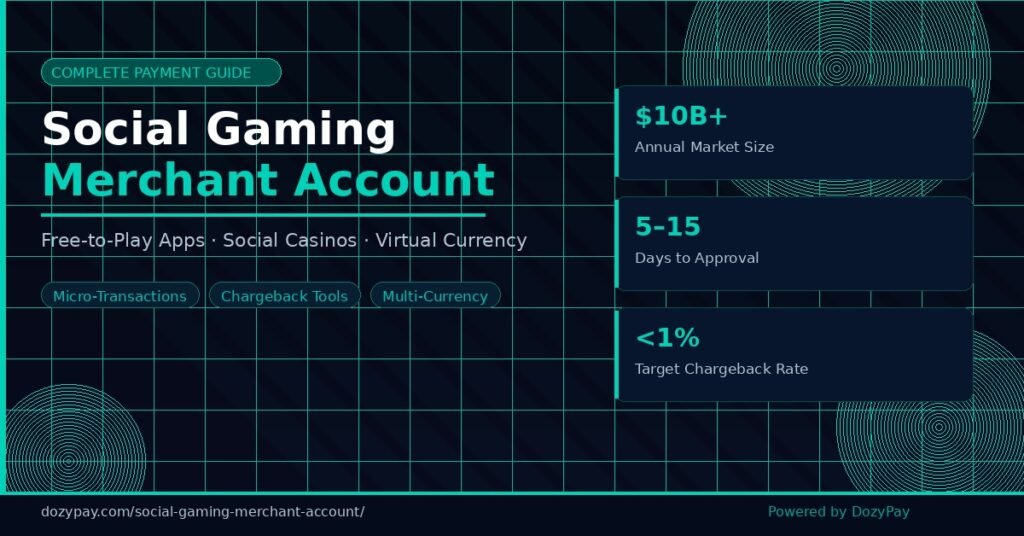

If you operate a social casino app, a free-to-play gaming platform, or a virtual currency marketplace, getting your payments infrastructure right is one of the most consequential decisions you will make. Yet the questions that matter most — about approval, chargebacks, processing fees, compliance, and what distinguishes a social gaming merchant account from a standard one — rarely have clear, consolidated answers.

How This FAQ Is Structured?

Specifically, this FAQ compiles the 13 most important questions DozyPay receives from app developers, social casino founders, and virtual currency platforms. Furthermore, every answer is written to give you operational clarity — not vague reassurances — so you can make informed decisions about your payment setup.

Before diving in: if you are still weighing your options, our Social Gaming Merchant Account Complete Payment Guide covers the full landscape in detail.

Q1: What exactly is a social gaming merchant account, and how is it different from a standard merchant account?

A social gaming merchant account is a specialised payment processing account configured for platforms where players purchase virtual currency, in-app items, or premium features — but do not win real money. Specifically, because regulators and acquiring banks treat social gaming differently from both e-commerce and real-money gambling, these accounts require specific MCC (Merchant Category Code) classification, custom chargeback thresholds, and often multi-currency processing capability that standard accounts cannot provide.

Moreover, the core difference is risk classification. Standard merchant accounts assume low-risk transaction patterns. However, a merchant account for social gaming must be underwritten to handle high transaction velocity, microtransaction volumes, a demographically broad cardholder base, and the chargeback patterns that are common in gaming — all of which fall outside the parameters of a generic account.

Q2: How does payment processing for social gaming apps actually work end-to-end?

Payment processing for social gaming apps follows a specific flow that differs from standard e-commerce in several important ways. Consequently, understanding each stage helps you identify exactly where your merchant account configuration matters most:

- Player initiates a purchase — buying coins, gems, chips, or a premium subscription inside your app or web platform.

- Payment gateway tokenises the card — the gateway captures the card data, tokenises it, and then routes the transaction to the appropriate acquiring bank via the card network (Visa/Mastercard).

- Acquirer checks against your merchant account profile — the transaction is validated against your approved volume, MCC, and risk parameters. This is where social gaming-specific underwriting matters most.

- Authorisation and settlement — approved transactions settle into your merchant account, typically within 2–5 business days depending on your processor and risk tier.

- Virtual currency delivery — your platform credits the player’s account with the purchased virtual goods. Importantly, this step must be independent of, and not contingent upon, any wagering or prize outcome.

Therefore, the distinction in step 5 is legally significant: social gaming payment processing remains permissible in most jurisdictions specifically because the virtual currency carries no real-money redemption value.

See also: Social Casino App Payment Methods 2026 for the full breakdown of accepted payment methods across platforms.

Q3: Is social gaming considered high-risk by acquiring banks and payment processors?

Yes — social gaming is classified as a high-risk vertical by most acquiring banks, even though it does not involve real-money gambling. In fact, the reasons are structural rather than judgmental:

- High chargeback rates relative to mainstream e-commerce, driven by impulse purchases, family account sharing, and player disputes about virtual item delivery

- Regulatory ambiguity in several jurisdictions, where the line between social gaming and gambling is actively contested

- High average transaction velocity — social gaming platforms can process thousands of microtransactions daily, which flags automated fraud risk algorithms

- Players cannot physically return virtual goods, which increases friendly fraud exposure

As a result, a social gaming payment solution high risk designation means that standard processors (Stripe, Square, PayPal) will either decline your application outright or place your account under restrictive rolling reserves and volume caps. Therefore, working with a specialist social gaming merchant account provider who has established relationships with high-risk acquirers is the practical solution.

Related: Social Gaming vs Real Money Gambling Merchant Account — Key Differences

Q4: What documents does a social gaming merchant account provider typically require for approval?

Typically, underwriting requirements vary between processors. However, underwriters consistently require the following documents for social gaming merchant account applications:

- Certificate of Incorporation and business registration documents

- Proof of beneficial ownership (for all owners with 25%+ shareholding)

- A completed and signed merchant application form

- Three to six months of prior processing statements, if available

- A detailed description of your platform — specifically how virtual currency is acquired, used, and whether any real-money redemption pathway exists

- Terms of Service and Refund Policy URLs

- Screenshots or a live demo of your app/platform checkout flow

- Proof of PCI DSS compliance or your current compliance status

- A voided cheque or bank letter for settlement account verification

For new operators without processing history, underwriters will place heavier weight on your business plan, platform architecture, and founding team’s track record. Additionally, a clean compliance posture at application significantly improves approval speed.

Q5: What is a realistic approval timeline for a social gaming merchant account?

Specifically, for a social gaming merchant account — as opposed to a real-money gambling account — realistic timelines are as follows:

| Account Type | Typical Approval Time | Key Variables |

| Social gaming (established platform) | 5–10 business days | Prior processing history, clean chargebacks |

| Social gaming (new launch) | 10–21 business days | Business plan quality, compliance docs |

| Mobile social gaming merchant account | 7–14 business days | App store integration, IAP structure |

| Virtual currency platform | 10–21 business days | Currency model, redemption policy clarity |

Delays most commonly occur due to incomplete documentation, unclear virtual currency redemption policies, or unresolved compliance gaps. Furthermore, partnering with a processor that specialises in iGaming significantly shortens back-and-forth review cycles.

Q6: How should a mobile social gaming merchant account be structured differently from a web platform account?

In particular, a mobile social gaming merchant account needs to account for the distinct payment flows, revenue share agreements, and compliance obligations that apply to app-based transactions:

- Purchases made through iOS App Store or Google Play are governed by Apple and Google’s payment systems — your merchant account consequently covers web checkout and alternative payment methods outside the native app stores.In-App Purchase (IAP) processing:

- Mobile payment SDKs must achieve PCI DSS certification and pass testing across operating system versions to prevent dropped transactions.SDK integration requirements:

- Mobile users expect to purchase in their local currency. Additionally, your mobile social gaming merchant account should support dynamic currency presentation at checkout.Multi-currency at the local level:

- Mobile platforms generate higher friendly fraud rates due to family account sharing and child purchases. Your account must therefore include velocity controls and 3DS2 authentication.Heightened chargeback monitoring:

- If you process outside the app stores, your merchant account revenue does not carry the 15–30% platform fee — this has direct implications for your processing fee economics.App store split awareness:

For a full breakdown of mobile payment infrastructure, read: Mobile Social Gaming Payments: In-App Purchase Processing for iOS & Android

Q7: What chargeback rate is considered acceptable for social gaming platforms, and how do you manage it?

Visa and Mastercard set the standard chargeback threshold at 1% of monthly transaction count. Specifically, for social gaming platforms, staying below 0.6% is the pragmatic target — processors typically begin enhanced monitoring programmes at 0.75–0.85%, and account suspension risk rises sharply above 1%.

The most effective chargeback management strategies for social gaming merchant accounts are:

- Implement 3DS2 authentication on all card transactions — this shifts liability to the issuing bank on authenticated transactions

- Additionally, use clear, recognisable billing descriptors that players will recognise on their card statement (e.g. ‘DOZYPAY*GAMENAME’ rather than a cryptic processor code)

- Respond to Retrieval Requests within 10 days without exception — most platforms that exceed chargeback thresholds fail at this stage

- Deploy velocity rules: flag and review accounts that make 3+ purchases within a 10-minute window

- Furthermore, maintain detailed transaction logs with device fingerprinting data — this is your primary evidence in chargeback representment

- Offer a frictionless refund path: platforms that make refunds difficult see higher chargeback conversion rates from dissatisfied players

See our detailed guide: How to Reduce Chargebacks on a Casino Merchant Account

Q8: How does virtual currency processing work within a social gaming merchant account, and what compliance rules apply?

Virtual currency within a social gaming context — coins, gems, chips, tokens, or any non-redeemable digital unit — is something payment networks treat as a digital good purchase, not as a financial instrument. Specifically, this distinction is what allows most jurisdictions to permit social gaming payment processing without requiring a gambling licence.

The compliance rules that apply are:

- Virtual currency must have no pathway to real-money conversion, cash withdrawal, or transfer to other players for real value. Any such pathway converts your platform into a real-money gambling operator in the eyes of most regulators.Non-redeemability requirement:

- Your Terms of Service must explicitly state that purchased virtual currency is non-refundable after use and carries no monetary value.Clear purchase terms:

- Depending on jurisdiction, your platform must implement age gates or full age verification at account registration — not just at the point of purchase.Age verification:

- Additionally, while social gaming is not subject to the same AML obligations as licensed gambling, platforms with high-value virtual currency transactions should maintain KYC processes for high-spend accounts.AML compliance:

- In several jurisdictions, virtual currency sales attract VAT or digital services tax. Consequently, your merchant account must generate compliant tax records for each transaction.Tax treatment:

Related: Virtual Currency Merchant Account: GameFi & Social Casino App Purchases

Q9: Which payment methods should a social gaming payment solution support in 2026?

In 2026, a comprehensive social gaming payment solution should support the following method categories:

- — still the primary purchase method for desktop and web-based social gaming.Credit and debit cards (Visa, Mastercard, Amex where available)

- — high conversion rate on mobile due to one-tap checkout.Digital wallets (PayPal, Apple Pay, Google Pay)

- — a growing segment, particularly for high-spend accounts seeking to avoid card fees. Additionally, ACH reduces your per-transaction processing cost significantly.Bank transfers and ACH/eCheck

- — increasingly expected by crypto-native social gaming demographics.Cryptocurrency (Bitcoin, Ethereum, USDC stablecoins)

- — valuable for underage-adjacent demographics and players without bank accounts.Prepaid cards and vouchers

- — emerging in casual and mid-core social gaming, particularly Klarna and Afterpay.Buy Now Pay Later (BNPL)

Therefore, the key principle for method selection is matching your player demographics to payment preferences by market. For example, a social gaming platform targeting Southeast Asia will have a very different optimal payment mix than one targeting North America or Western Europe.

Read: ACH & eCheck for Gambling Platforms — Beyond Card-Only Processing and Casino Payment Gateway Cryptocurrency: Bitcoin, Ethereum & Stablecoins

Q10: What processing fees should a social gaming merchant account expect, and what drives them up or down?

As expected, processing fees for social gaming merchant accounts run higher than standard e-commerce rates because of the high-risk classification. The typical fee structure breaks down as follows:

| Fee Component | Typical Range for Social Gaming |

| MDR (Merchant Discount Rate) | 2.8% – 4.5% per transaction |

| Rolling reserve | 5% – 10% held for 90–180 days |

| Chargeback fee | $20 – $40 per dispute |

| Monthly account fee | $50 – $200 depending on processor |

| Setup / onboarding fee | $0 – $500 (varies widely) |

| High-volume discount threshold | Typically available above $100k/month |

Specifically, the factors that push your rates down over time include: a consistent chargeback ratio below 0.5%, stable processing volume above $50k/month, 12+ months of clean processing history, and PCI DSS Level 1 or Level 2 compliance. Additionally, the fastest way to negotiate lower rates is to bring competing processor quotes to your renewal conversation.

More: How to Get a Low-Fee Gambling Payment Gateway

Q11: What are the most common reasons social gaming platforms get their merchant accounts terminated, and how do you avoid them?

In practice, account terminations in the social gaming vertical almost always stem from one of five root causes:

- Sustained monthly chargeback rates above 1% trigger card network monitoring programmes (Visa VAMP, Mastercard ECM) and often result in termination or forced reserve increases.Chargeback ratio breach:

- Additionally, adding any real-money redemption pathway, crypto-for-cash conversion, or P2P transfer without disclosing this to your processor constitutes material misrepresentation and grounds for immediate termination.Undisclosed business model changes:

- If your platform processes 3x your approved monthly volume without prior notification, processors may freeze funds and close the account as a risk control measure.Processing volume far exceeding approved limits:

- Furthermore, a licensing dispute, regulatory investigation, or significant negative press coverage in a key market can trigger a processor’s risk review and termination.Regulatory action or adverse media:

- If a breach occurs and you lack compliance status, your acquiring bank faces significant liability and will consequently terminate the account immediately.PCI DSS non-compliance:

Therefore, the practical safeguard for all five risks is proactive communication with your payment processor. Notify them of material business model changes, volume spikes, and any regulatory contact before they discover it independently.

Q12: Can a single merchant account for social gaming handle multiple games, platforms, or geographies?

In most cases, yes — a single social gaming merchant account can handle multiple games or sub-brands under one merchant umbrella, provided the underlying business entity is the same. However, there are important structural considerations to review before consolidating everything under one account:

- — recommended for billing descriptor clarity and chargeback isolation.Separate DBA (Doing Business As) names per game title

- — Additionally, this must be explicitly enabled. Do not assume that approval in one currency extends to all geographies automatically.Multi-currency processing

- — certain countries may be excluded from your merchant account based on your acquiring bank’s licence or regulatory restrictions in that market.Jurisdictional restrictions

- — running all games through one account means one chargeback spike on one title can affect your entire processing capability. As a result, some operators use separate accounts per high-volume title as a risk isolation strategy.Volume aggregation risk

Ultimately, a specialist social gaming merchant account provider can help you architect the right account structure — single account with sub-descriptors, or a multi-MID setup — based on your platform’s risk and volume profile.

Q13: What should I look for when choosing a social gaming merchant account provider, and why does provider specialisation matter?

Ultimately, choosing the right social gaming merchant account provider is as important as the payment infrastructure itself. In particular, here is the evaluation framework DozyPay recommends:

- Does the provider have active social gaming clients — not just ‘gaming’ in general? Specifically, regulatory knowledge, acquirer relationships, and risk models differ substantially between real-money gambling and social gaming.Vertical specialisation:

- A provider with multiple acquiring bank relationships gives you redundancy. Additionally, if one acquirer exits the social gaming vertical (as has happened several times in the past decade), you retain processing continuity.Acquirer relationships:

- Does the provider offer built-in chargeback alerting, automated responses, and representment support — or do you manage this entirely yourself?Chargeback management tools:

- Furthermore, as your platform scales internationally, your provider must support the currencies and payment methods of your growth markets without requiring a new merchant account in each jurisdiction.Multi-currency and multi-geography capability:

- Avoid providers that obscure fees in long-term contracts or bury reserve terms in small print. A trustworthy social gaming payment solution provider will show you the full fee schedule before you sign.Transparent fee structure:

- Finally, review the documentation for the payment gateway API. Poor integration quality and underdocumented SDKs create ongoing engineering costs that dwarf the savings from a lower processing rate.Integration quality:

DozyPay specialises exclusively in high-risk iGaming payment solutions — including social gaming, real-money casino, sports betting, and virtual currency platforms. Consequently, our acquiring relationships, chargeback tooling, and compliance infrastructure are built specifically for this vertical.

Explore: Social Gaming Merchant Account — Full DozyPay Overview and Social Gaming Payment Mistakes to Avoid

Final Notes for Social Gaming Operators

Ultimately, getting your payment infrastructure right is not a one-time decision — it is an ongoing operational discipline. Furthermore, the platforms that maintain healthy social gaming merchant accounts over the long term are the ones that treat chargeback management, compliance documentation, and processor communication as live business functions rather than setup tasks.

In summary, whether you are launching a new social casino app, scaling a virtual currency marketplace, or restructuring an existing payment setup that has hit friction, the questions above cover the issues that most commonly determine whether a social gaming operator processes smoothly or faces account instability.

For a full consultation on your social gaming payment setup, visit DozyPay Social Gaming Merchant Account and speak with a specialist.

Related Reading from DozyPay

- Social Gaming Merchant Account — Complete Payment Guide

- Social Gaming vs Real Money Gambling Merchant Account

- Social Gaming Payment Mistakes

- How to Accept Credit Cards on a Social Gaming Website

- Virtual Currency Merchant Account: GameFi & Social Casino

- Mobile Social Gaming Payments: iOS & Android

- Social Casino App Payment Methods 2026

Payment Gateway vs Merchant Account for Online Casino